Coffee - Commodity Profile - DA

The Philippines was once a reliable source of good quality Robusta from the late 1970’s to the early 1990’s (NCDB).The Philippines’ consumption from 1993-1995 was 48,000 tons. It has already reached 55,000 MT in 2004. While instant coffee is still the general preference, the ground and brew sector is growing. Organic coffee is the other growth area that the industry can look forward to.

Description

• The country has two most popular varieties of coffee: Coffea arabica, otherwise known as arabica, and Coffea canephora, or robusta.

• Based on statistics from the International Coffee Organization, robusta accounts for 75% of the country’s total production and Arabica, 5-10%.

• Other varieties such as excelsa and liberica, also, thrive in the country and accounts for 15-20% of the country’s coffee produce.

Production

• World coffee production in 2004 is 6.81 M mt or 113,479,000 60-kg bags up by 9.75% from 2003 but is still much lower than the production in 2002 of 7.32 M mt, the highest production in decades.

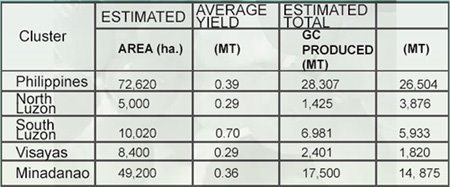

• The top producing countries in 2004 are Brazil (2.3 M mt of Arabica), Vietnam (0.90 M mt of Robusta), Colombia (0.63 M mt of Arabica) and Indonesia (0.34 M mt of Robusta)• Based on the data of Nestle the total productive coffee area in the country is about 72,620 hectares with 49,200 hectares in Mindanao.

• The average yield is only 0.39 mt/ha but the potential is 2-3 mt/ha given the right management.

• It is estimated that around 300,000 Filipinos depend on the coffee industry.

Estimated Production, 2003-04 (Nestle)

(See table from the website)

Processing

• Aside from the instant coffee players such as Nestle, URC and San Miguel there are other players in the market such as Kopiko and Kape Filipino,

• In the ‘Ground and Brew’ the signi. cant players in the local market are Figaro, Monk’s Blend, Café Amadeo, Batangas Brew

• Available also in wet markets are roasted beans of robusta and liberica for grinding

Cost and Return

• In Cavite total cost of production is P27,461.50/ha if with fertilization on a yield of 1000 kg/ha and P15,000.00/ha if without fertilization on a yield of 400 kg/ha green bean

• In Sultan Kudarat the cost of production for Robusta is around P27/kg as monocrop and P23/kg with intercrops.

• Net income is P20-30,000/ha at P43/kg green bean

Demand and Supply Projections

• Domestic demand stands at 55,000 MT

• Domestic production is around 27,000 MT in 2004

• The shortfall of 30,000 MT is imported at a total of US$ 25 M/yr

• Local demand is growing at 3%/year to about 65,693 tons by 2010 and 78,439 tons by 2015

• The country will be importing 46, 000 tons by 2010 at the present rate

• In terms of expansion area for coffee Mindanao has enough area to answer for about 70% of the projected 10,000-hectare per year expansion needed to be self suf. cient

• There is also an increasing local demand for organically grown coffee and other specialty coffee such as Phil. Barako Coffee, Halal Coffe, Phil. Excelsa Coffee and Kape Alamid

Local Market

• Nestle has about 80% of the market

Foreign Market/Trade

• Top exporting countries in 2004 are Brazil (1.58 M mt), Vietnam (0.89 M mt), Colombia (0.61 M mt) and Indonesia (0.27 M mt)

• The Philippines exported $4.51 M worth of coffee products. Liberica and Excelsa accounted for $0.14 M

• In 2004 the Philippines imported 15,087 mt of raw green beans, roasted beans and extracts worth USD 25.49 M

• Robusta green bean import in 2004 was 8,196.4 mt at $ 7.63 M or $0.93/kg• Arabica green bean import in 2004 was 81.34 mt at $1.144/kg

Marketing Practices

• Farmers generally dry their coffee beans and have them milled through local millers.

• Green beans are sold to traders or directly to the buying stations of Nestle or to wet markets

Problems

• low production,

• low income of coffee farmers,

• poor quality of coffee beans,

• lack of postharvest facilities for quality processing,

• highly . uctuating market prices

Price Trend

• Prices of Robusta is highly volatile- P43/kg in March 2005 and P70/kg in July 2005

• Arabica is higher at up to P110/kg

Credit Assistance

• Quedancor- Self-reliant Team (SRT), P28,000/ha for rehabilitation maximum of P50,000/farmer

• Land Bank of the Philippines- P45,000/ha for rejuvenation, P60/ha for new plantings

Investment Opportunities

• Credit facilities for rehabilitation- P300 M• Nurseries for seedlings of Robusta, Arabica and Liberica

• Coffee plantations for robusta, Arabica and liberica• Post harvest facilities • Processing for the ground and brew

Institutional Support

• A priority commodity under HVCC

• National Coffee Development Board

• Cavite State University

• Benguet State University

http://www.da.gov.ph/mindanao/com_profile/coffee.html

posted by GeorgeM @ 3:26 AM

![]()

0 Comments:

Post a Comment

<< Home